Is Affirm Legit? A Deep-Dive Review of Safety, Fees, Credit Impact, and What Shoppers Should Know

Wondering if Affirm is legit? Learn how it works, how safe it is, how it affects credit, fees/APR, scams to avoid, and who should use it.

.avif)

Buy Now, Pay Later (BNPL) has become a normal checkout option—especially for online shopping. And Affirm is often one of the first names you’ll see next to the “Pay in installments” button. That visibility brings a fair question:

Is Affirm legit—or is it a trap?

Affirm is a real, established BNPL lender that works with major merchants and has formal security programs, policies, and disclosures. But “legit” doesn’t automatically mean “risk-free” or “best choice for everyone.” Some shoppers love the flexibility. Others run into issues with refunds, customer support, payment disputes, or overextending their budgets.

This guide breaks it all down in plain language: how Affirm works, what makes it legitimate, how safe it is, how it can affect your credit, common complaints, and how to use it responsibly—especially if you’re shopping online.

What is Affirm?

Affirm is a BNPL provider that offers installment payment plans at checkout. Instead of paying the full purchase price upfront, you split the cost into smaller payments over time.

Affirm typically offers:

- Short installment plans like Pay in 4 (often interest-free, depending on the merchant and eligibility)

- Longer monthly installment plans that may charge interest (APR can vary, and some plans can be high)

You’ll most commonly see Affirm at checkout on partner sites, but you may also be able to use it more broadly through their app and virtual card options depending on location and eligibility.

Is Affirm legit?

Yes—Affirm is legitimate. It’s not a scam company posing as a lender. Here’s what supports that legitimacy:

It’s widely reviewed and used as a BNPL lender

Major consumer finance reviewers explain Affirm’s product as a BNPL installment loan with clear disclosures at checkout, typically with no “junk fees” like late fees.

It publishes detailed security and fraud-prevention guidance

Affirm maintains a security program and also provides consumer-facing education about fraud tactics like phishing and social engineering. It also follows secure development practices, including regular sast scan processes, to identify and address potential vulnerabilities in its systems.

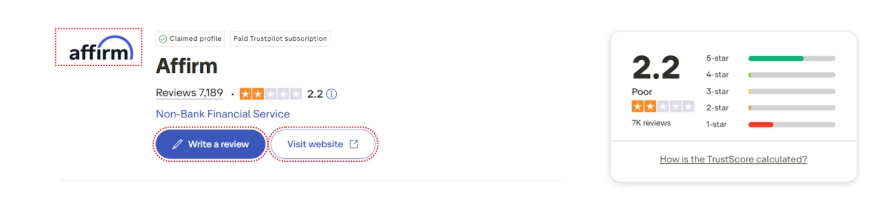

It has real customer feedback—both positive and negative

Affirm has a large volume of real user feedback online, which is helpful when you’re trying to judge whether a company is legitimate or just good at marketing. One of the most referenced sources is Affirm reviews on Trustpilot, where the platform currently shows an overall star rating of 2.2 out of 5 stars based on thousands of reviews (and you’ll find everything from detailed praise to serious complaints).

What stands out is the pattern: people who use Affirm for simple purchases and repay on time often report a smooth experience, while many negative reviews focus on customer support delays, refund timelines, disputes, and payment/account issues.

Important nuance: a company can be legitimate and still frustrating to deal with sometimes. Most “Is it legit?” questions are really two questions:

- Is this a real company offering a real financial product? Yes.

- Will the experience always be smooth and customer-friendly? Not necessarily.

Is Affirm safe to use?

Generally, Affirm is considered safe as a payment option, especially when used responsibly and through official channels.

Security-focused reviewers describe Affirm as “generally safe,” while also pointing out risks BNPL users should understand—like weaker protections compared with traditional credit cards in some situations and potential credit impacts if payments are missed.

What “safe” means here (and what it doesn’t)

Affirm also runs a formal security program shaped by common industry frameworks and standards.

Safe can mean

- You’re not handing payment details to a random, unverified site

- The company has security practices, policies, and monitoring

- There are official processes to report scams and suspicious outreach

Safe does NOT mean

- You can’t overspend

- Refunds will always be instant

- You’ll never run into customer support issues

- There’s no chance of credit score consequences

How Affirm works (step-by-step)

If you’ve never used Affirm, here’s the typical flow:

1) Choose Affirm at checkout

On a supported merchant site, you select Affirm as the payment method.

2) Pick a payment plan

You may see multiple options—shorter installment plans (like Pay-in-4) or longer monthly plans.

3) Apply and get a decision

Approval depends on eligibility checks (which may vary by plan and user profile). You’ll be shown the terms before you finalize.

4) Make payments over time

Payments are due on the schedule in your agreement. Affirm emphasizes transparency—showing the total cost, interest (if any), and payment timeline upfront.

Fees, APR, and the real cost of using Affirm

One reason Affirm became popular is the promise of clear terms and fewer surprise fees.

Does Affirm charge late fees?

Many mainstream reviews note that Affirm is known for having no late fees, which is a big difference compared to many credit cards.

But “no late fees” doesn’t mean “no consequences.” Missing payments can still create problems (more on that in the credit section).

What APR does Affirm charge?

This is where shoppers get tripped up.

Some plans are 0% APR, but others can be significantly higher. NerdWallet’s review notes that monthly payment plans may charge up to 36% APR.

So the same checkout option can be:

- a helpful 0% installment plan for one person

- an expensive loan for another person

What determines your APR?

APR is influenced by factors like:

- the merchant offer (some subsidize 0% promotions)

- your eligibility profile

- purchase amount and repayment term length

Rule of thumb: the longer the repayment period, the more likely interest becomes part of the deal.

Does Affirm affect your credit score?

It can—depending on the type of plan, your payment behavior, and how the loan is handled or reported.

If you pay on time

Paying on time helps you avoid negative marks and keeps your account in good standing. Some plans may not show up the same way as a traditional credit product, but your agreement is still a loan.

If you miss payments

Missed or late payments can limit your ability to get new plans and may affect credit outcomes. Security.org explicitly warns about potential credit impacts as part of BNPL risk.

A recent news/business report also noted Affirm’s own messaging that missed/late payments can affect credit.

Why BNPL credit rules have been under scrutiny

BNPL has drawn regulator attention around consumer protections, dispute rights, and consistent treatment compared to credit cards. The CFPB previously issued an interpretive rule aimed at applying credit-card-like protections to BNPL, as covered by the CFPB and major media.

There have also been policy shifts and legal/regulatory back-and-forth in the BNPL space since then (including changes noted in CFPB compliance resources).

Practical takeaway: BNPL is not “just a payment button.” It’s still credit-like, and missed payments can have real consequences.

The biggest risks people run into with Affirm

Let’s get very specific. Most Affirm problems fall into a few repeat categories:

1) Overspending because the payment looks small

This is the classic BNPL trap: $35 today feels manageable—until you have four different BNPL plans running at the same time.

BNPL apps like Affirm focuses heavily on how installment framing can encourage buying things you wouldn’t purchase outright.

2) Refund and return confusion

Refund flows can be messy with any financing product. The merchant, the lender, and the payment schedule all have to reconcile.

This is one reason regulators have focused on ensuring consumers can dispute charges and obtain refunds in a way that resembles credit card protections.

3) Dispute protections aren’t always as intuitive as credit cards

BNPL may not always match “credit card-level protection” in practice, which matters if something goes wrong with a purchase.

4) Customer support complaints

A large chunk of negative sentiment around Affirm is service-related: difficulty resolving a billing issue, frustration with communication, or slow resolutions.

(That doesn’t mean every shopper has this experience—but it’s common enough to treat it as a real factor.)

How to avoid Affirm scams and fake messages

A lot of people get scammed by imposters, not by the real Affirm.

Affirm explicitly warns about phishing and social engineering—fraudsters pretending to be Affirm via email, text, or calls to trick users into sharing sensitive info.

Use this “anti-scam” checklist

If you want to use Affirm safely, follow this every time:

- Only log in via the official site/app: use Affirm’s official website or the official mobile app

- Don’t click login links in random emails/texts (even if they look real)

- Never share one-time passcodes with anyone

- Check the sender domain carefully (scammers use near-identical lookalikes)

- Report suspicious outreach using Affirm’s official guidance

Real-world scenarios: when Affirm is a good idea (and when it isn’t)

Affirm can be genuinely helpful in specific situations—especially when it saves you cashflow stress without adding extra cost. But it can also become expensive (or messy) when it’s used as a “budget shortcut.” Here are real-life examples to make the decision clearer.

Affirm can be smart when…

- You get a 0% APR plan and you were already planning to buy the item

- You have stable cash flow and you can automate payments

- You’re using it for a necessary purchase (replacement laptop, appliance, or work gear) and you’ve compared alternatives

Affirm is usually a bad idea when…

- You’re using it to “make the checkout pain go away”

- You’re stacking multiple BNPL plans across different apps

- You’re using longer-term high-APR financing when a lower-interest option exists

- You’re already struggling to keep up with bills

If your goal is financial stability, BNPL should be a tool—not a habit.

Affirm vs credit cards: what’s actually better?

This depends on your situation, but here are the practical comparisons shoppers care about.

Where Affirm can beat a credit card

- Clear “total cost” view upfront (especially if 0% APR applies)

- No late fees (in many cases)

- Predictable payoff schedule

Where a credit card can beat Affirm

- Stronger dispute and chargeback expectations in many people’s minds (and often smoother processes)

- Rewards points/cashback

- Some cards offer 0% intro APR promos too

Because BNPL consumer protections have been evolving and debated, it’s worth paying attention to official guidance and changes over time.

What merchants should know about Affirm (especially in ecommerce)

If you’re running an online store, BNPL is more than a payment method—it’s part of conversion psychology.

From a merchant perspective, BNPL can:

- increase conversion rate by lowering perceived purchase friction

- lift average order value (AOV) because customers “feel” the smaller payment

But it can also:

- increase customer service volume (refund timing confusion, installment questions)

- attract higher return rates in certain categories (because shoppers buy more impulsively)

For ecommerce sellers building a brand and customer trust—especially those sourcing products, building bundles, and optimizing checkout on Spocket—the best approach is to treat BNPL as an option, not the headline. Make sure your refund policy is clear, your shipping times are transparent, and your product pages reduce buyer’s remorse.

Common Affirm complaints (and what they usually mean)

To keep this realistic, let’s interpret the most common complaint themes you’ll see in consumer reviews.

“Affirm ruined my credit”

Often tied to missed payments, misunderstandings about whether a plan is “credit,” or confusion about reporting. BNPL can affect credit outcomes when things go wrong.

“My refund is taking forever”

Refund timing can involve both the merchant and the loan schedule. This is a known friction point across BNPL—and a reason regulators highlighted dispute/refund rights.

“Customer support won’t help”

Customer service dissatisfaction is a frequent theme in large public review sets.

Tip: If you’re considering Affirm, read the 1–3 star reviews specifically. They usually reveal the real edge cases: returns, disputes, identity verification, and payment scheduling.

How to use Affirm responsibly (practical rules)

If you decide to use Affirm, these rules reduce your risk dramatically:

Keep it to one plan at a time

BNPL becomes dangerous when you stack it. One plan = manageable. Five plans = chaos.

Treat the installment as a “must-pay bill”

Don’t think “I’ll handle it later.” Put payment dates in your calendar and turn on autopay.

Prefer 0% APR offers

If you’re paying interest, compare alternatives:

- credit card 0% intro APR

- a lower-interest personal loan

- saving for 2–4 weeks and paying upfront

Don’t use Affirm for return-prone categories

If you often return fashion items (size issues) or electronics (compatibility issues), consider payment methods that make disputes and refunds simpler.

Watch out for phishing

Use official channels only and follow Affirm’s security guidance on spotting scam outreach.

Final verdict: Is Affirm legit?

Yes—Affirm is legit. It’s a real BNPL provider with published security practices, widely documented product terms, and a large consumer footprint.

But it’s not “free money,” and it’s not automatically the smartest way to pay.

If you:

- choose a low- or 0%-APR plan,

- keep purchases within budget,

- automate payments,

- and stay alert to phishing scams,

then Affirm can be a convenient tool for splitting costs.

If you’re using it to stretch spending, stacking multiple BNPL plans, or relying on long-term high APR offers, it can become expensive and stressful fast.

Start your dropshipping business today

FAQs about Affirm’s Legitimacy

Is Affirm legit or a scam?

Affirm is legit—a real BNPL lender used by many merchants and shoppers. Scam attempts are usually imposters using fake emails/texts. Use Affirm’s official website to avoid lookalikes.

Is Affirm safe for debit cards or bank accounts?

Affirm is generally considered safe as a platform, and it maintains a formal security program and consumer guidance. Still, you should follow basic account security best practices and avoid phishing links.

Can Affirm hurt your credit?

It can—especially if you miss payments. Reviews and reporting note BNPL risk includes credit impact when payments are late or missed.

Does Affirm charge hidden fees?

Mainstream reviews commonly emphasize no late fees and clearer disclosures than many alternatives. However, interest (APR) can apply on some plans, and that cost can be significant depending on the offer.

Can you pay off Affirm early?

Yes—many Affirm plans allow early payoff, which can help you reduce overall interest costs on plans that charge APR. Before doing it, check your loan details in the Affirm app/account to confirm how payoff is applied and whether it changes the total you owe.

Launch your dropshipping business now!

Start free trial

Related blogs

.avif)

AliExpress vs. Spocket: Is Spocket Better Than AliExpress?

Compare AliExpress and Spocket to see which dropshipping platform offers better shipping, supplier reliability, product quality, and growth potential.

Dripshipper Reviews: Is This Coffee Dropshipping Platform Worth It?

Read this detailed Dripshipper review covering features, pros, cons, pricing, customer feedback, profitability, and better dropshipping alternatives.

Is BigBuy Legit? Honest Review for Dropshipping Businesses

Find out if BigBuy is a reliable dropshipping supplier, including its features, pros, cons, pricing concerns, reviews, and alternatives for ecommerce sellers.